The statements made and opinions expressed in this publication are solely the responsibility of the author(s) and do not necessarily reflect the opinions of the Security in Context network, its partner organizations, or its funders.

By Andrei Guerrero and Jorge Carrillo

This paper was prepared for the online conference, The China Effect: Rethinking Development in Latin America and the Caribbean, that took place on December 3, 2025, and organized by the University of Oklahoma Center for Peace and Development, the Security in Context Network (SiC), and the Center for Chinese Mexican Studies (Cechimex) and the School of Economics at the National Autonomous University of Mexico (UNAM).

Andrei Gurrero is a professor and researcher at the Autonomous University of Baja California (UABC), Tijuana campus. Member of the Latin American and Caribbean Academic Network on China (Red ALC-China).

We note with sadness that our coauthor, Jorge Carrillo, passed away after the paper was largely completed. He was a great scholar and mentor, and made important contributions to this work. We are grateful for the opportunity to have collaborated.

Citation: Guerrero, Andrei & Carrillo, Jorge, 2026. “Electromobility and Technological Rivalry: Mexico in the China-United States Confrontation,” Security in Context Research Paper 26-04. May 2026, Security in Context.

Abstract: This chapter analyzes the reconfiguration of the automotive industry in the context of the transition to electromobility and the growing technological rivalry between China and the United States, positioning Mexico as an intermediary space highly conditioned by these dynamics. It argues that the sector is undergoing three simultaneous processes: a shift in production toward China, Mexico, and other Asian economies; the technological transformation driven by electric vehicles; and the increasing politicization of trade and investment under national security criteria. China has consolidated its global leadership through a long-term strategy based on active industrial policies, vertical integration, and control of key segments of value chains (especially batteries). In response, the United States has adopted a protectionist approach that combines tariffs, technological restrictions, and regulatory measures, expanding its concept of national security to include control of critical inputs and production capabilities. This confrontation is reshaping global supply chains and generating indirect effects on the integration of the Mexican sector analyzed here. The study shows that Mexico, despite its importance as an export platform under the United States-Mexico-Canada Agreement (USMCA), remains deeply dependent on the US market, which limits the expansion of the Chinese automotive industry. China's presence, meanwhile, is fragmented, focusing on the domestic market and exhibiting limited production capacity, resulting in a conditional integration rather than an expansion with autonomous capabilities. It concludes that Chinese participation in Mexico does not represent an immediate threat of displacement, but rather a form of limited diversification, restricted by regulatory and geopolitical factors. Therefore, Sino-US competition and the technological transition toward electromobility create an environment of increasing uncertainty in Mexico, impacting the country's room for maneuvering.

Introduction

The automotive industry has entered a phase of transformation shaped by three simultaneous processes: a productive shift toward China, Mexico, and other Asian economies; a technological transition driven by the expansion of electric vehicles (EVs); and the growing politicization of trade and investment. These changes are not only reconfiguring the geography of production but are also reshaping the rules under which countries seek to integrate into global value chains (GVCs), in a context where considerations of economic and strategic security have become increasingly central to industrial decision-making.

With respect to electromobility, China has consolidated its position as the world’s leading producer and consumer of vehicles, as well as a dominant actor within automotive supply chains – particularly in electric batteries. This expansion is not limited to a quantitative increase in productive capacity; rather, it is underpinned by a process of vertical integration and technological upgrading that has altered the global balance of the sector. At present, China hosts six of the world’s largest lithium battery producers, accounting for more than 75 percent of global output (You, 2025). This group includes not only CATL but also national firms such as BYD, which surpassed Tesla in EV manufacturing and market leadership in 2025, producing 2.3 million vehicles compared to Tesla’s 1.6 million units (Ewing, 2026). This technological leadership has positioned electromobility as a central axis of international economic competition.

The United States’ response to these transformations has extended well beyond conventional trade instruments. Contemporary US industrial policy explicitly incorporates economic and national security considerations, translated into higher tariffs, extraordinary regulatory mechanisms, and sector-specific protection measures targeting the automotive industry and electric vehicles. In April 2025, the Trump administration announced the imposition of a 25 percent tariff on imports of automobiles and auto parts from China, invoking Section 232 of the Trade Expansion Act of 1962 – an instrument reserved for situations in which imports are deemed a potential threat to national security. As documented by the Congressional Research Service (2025), this measure reflects a clear shift toward a protectionist industrial strategy aimed at preserving strategic productive capacities in the face of foreign – primarily Chinese – competition. Within this framework, the expansion of tariff threats and regulatory uncertainty toward third countries has generated an environment of instability that extends beyond the US market to key trading partners such as Mexico and several European economies, while access to and control over critical inputs have become increasingly embedded in national security discourse.

Mexico occupies a particularly sensitive position within this context. As a key platform of the North American automotive industry under the USMCA framework, its economic integration is deeply conditioned by US market dynamics and policy decisions. In 2025, according to the National Institute of Statistics and Geography (INEGI), light-vehicle production in Mexico reached 3.9 million units, while exports totaled 3.3 million units, with the United States absorbing approximately 78.4 percent of total exports (García, 2026). At the same time, the Mexican domestic market has experienced a noticeable increase in the commercial presence of Chinese automotive brands, reflected in rising sales and imports during 2025. However, this expansion has not translated into a significant role in exports from Mexico to the United States, confirming that Chinese firms’ current integration remains concentrated in domestic consumption and component supply.

This coexistence fuels a narrative that portrays the expansion of the Chinese automotive industry in Mexico as a strategic threat to the US and, by extension, as a risk to the stability of the USMCA. Such narratives, however, contrast with the pragmatic and constrained nature of China’s presence in the country, which to date has been characterized by limited and fragmented forms of insertion, and is strongly shaped by the regional regulatory environment. From this perspective, the absence of fully integrated assembly plants operated by firms such as BYD and Changan illustrates this tension clearly. Despite earlier announcements and investment expectations, these companies have opted for operational models centered on vehicle imports or the assembly of semi-knocked-down kits, rather than the development of full manufacturing capabilities within Mexican territory. Rather than isolated cases, these dynamics reflect the structural limits facing Chinese automotive investment in North America within a context of strategic confrontation, accelerated electrification, and transnational political pressure. Although the presence of Chinese firms remains marginal compared to that of established multinational automakers operating in Mexico, their positioning and rapid expansion in domestic distribution channels point to a gradual, cautious, and highly conditional form of integration – one that still depends on US market access and industrial policy constraints.

Against this backdrop, this study analyzes the presence and trajectory of the Chinese automotive industry in Mexico as a geo-economic phenomenon shaped by recent conjunctural dynamics (2024-2025), including tariff escalation, the securitization of industrial policy, the accelerated transition toward electromobility, and specific political decisions. Adopting a triangular analytical perspective, the study examines the strategic rivalry between China and the United States alongside the margins of maneuver available to the Mexican state.

The chapter is organized as follows. The next section examines the global reconfiguration of the automotive industry and China’s leadership in electrification. The third section analyzes US industrial and national security policy in contrast to China’s cooperation-oriented strategy toward Latin America and the Caribbean (LAC), highlighting the role of critical inputs and their indirect implications for Mexico. The fourth section focuses on the presence of the Chinese automotive industry in Mexico, with particular emphasis on its structural constraints. The final section presents the conclusions and suggests that, instead of fostering decisive expansion, this presence has generated limited diversification in Mexico, marked by persistent dependence on the US market and an environment of increasing uncertainty.

The Reconfiguration of the Automotive Industry and China’s Productive Leadership

Over the past two decades, the automotive industry has experienced a gradual geographic reconfiguration. The historical leadership of the United States and Europe has been increasingly challenged – and in several segments surpassed – by the sustained rise of China as the world’s leading producer of electric vehicles (Figure 1). This transformation is not the result of chance; rather, it reflects a combination of conjunctural dynamics and deeper structural changes involving the relocation of industrial capacities and the incorporation of new economies into the global automotive system.

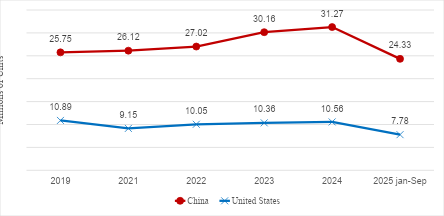

Figure 1: Automotive Production in China and the United States (Millions of Units): 2019-2025

Notes: The 2025 data only covers the months of January to September.

This shift has been gradual, but not slow. Between 2001 and 2008, China expanded its productive capacity by as much as 200 percent (Esparza, 2008). By 2009, it had become the world’s leading vehicle producer, and by the end of 2023 it had also achieved global leadership in passenger-vehicle exports (Cheng and Kubota, 2024). As shown in Figure 1, the People’s Republic of China (PRC) has nearly doubled US automobile manufacturing output. Between 2019 and 2024, this translated into a 22 percent increase for China and a 3 percent decline for its North American counterpart. Finally, the figure reveals that through the third quarter of 2025, Chinese production outpaced its counterpart by almost 213 percent. It also demonstrates that the shift in automotive productive leadership has not been merely cumulative but has accelerated in recent years, as the gap between China and the United States widened markedly in the post-pandemic period, reinforcing the perception of a structural transformation in the global automotive hierarchy.

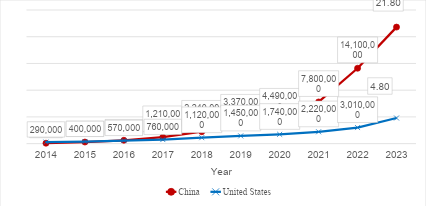

Along similar lines, in 2024 the PRC accounted for nearly 70 percent of global electric-vehicle production (IEA, 2025), reaching 21 million units in 2023 (Figure 2). China thus leads a sector oriented toward the development of clean technologies and characterized by a high degree of political and commercial contestation (Dupuis et al., 2024). The transition toward electromobility – hereafter also referred to as electrification – constitutes a central axis of the industry’s global reconfiguration, since, unlike previous technological shifts, it alters the final product, redefines global value chains, and reshapes both the cost structure and the technological requirements of the sector. Within this context, China has positioned itself as a dominant actor by securing control over strategic segments of the value chain, particularly battery manufacturing, as well as the extraction and processing of critical minerals and components.

Figure 2: China and the United States: Total EV Stock (Millions of Units): 2014-2023

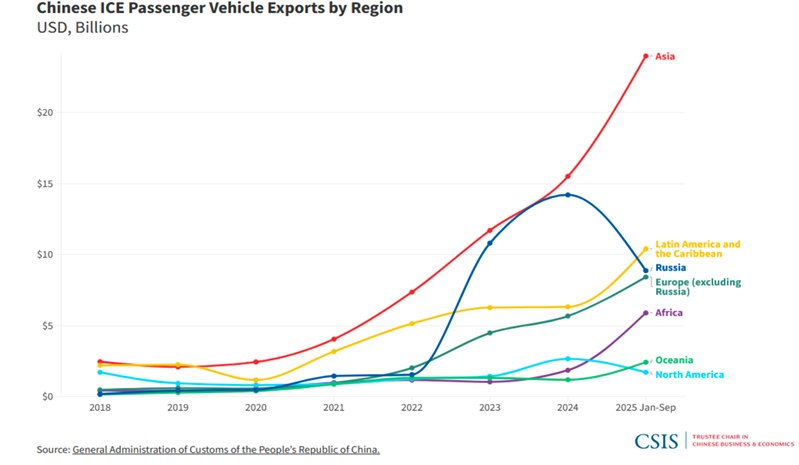

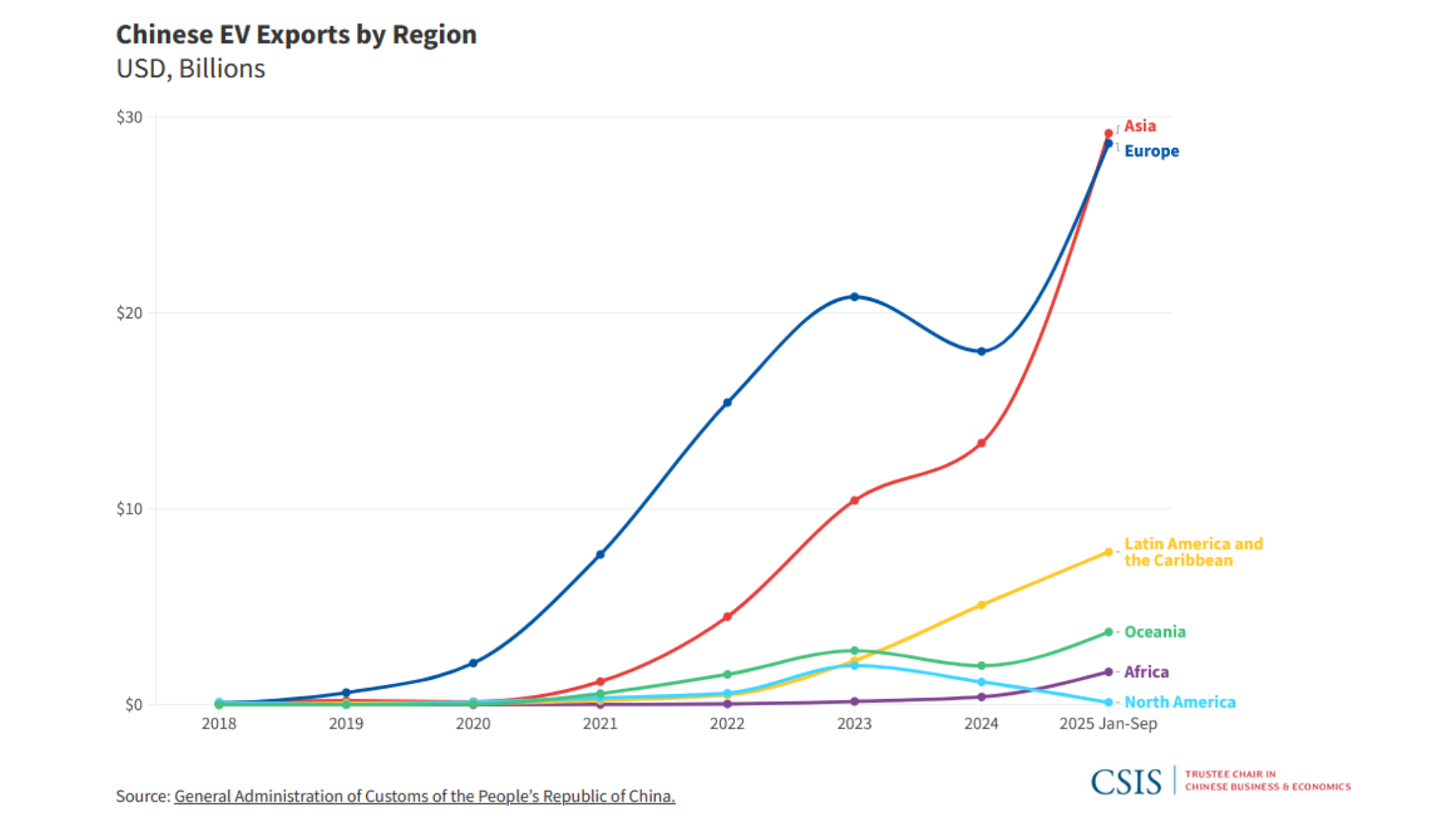

Accordingly, electromobility has ceased to be a strictly technological phenomenon and has become a structural driver of industrial competition, with direct implications for trade, investment, and global development strategies linked to the 2030 Agenda for Sustainable Development and the Paris Agreement, both of which emphasize the progressive reduction of global vehicular emissions. At the same time, the consolidation of China’s leadership is increasingly projected through its export capacity and its deepening integration into GVCs. This is evident not only in the rapid expansion of Chinese automotive exports – encompassing both internal combustion engine (ICE) vehicles and EVs – but also in the systemic articulation of production, technology, and trade, which has enabled the country to expand its presence in external markets and consolidate influence across strategic segments of the industry. Figures 3 and 4 confirm this trajectory, showing that Chinese ICE vehicle exports – particularly to Asia, where they approached USD 3 billion in September 2025 – have intensified markedly, while EVs exports to Asia and Europe have far outpaced those destined for other regions.

Figure 3: Exports of Chinese ICE Passenger Vehicles by Region (USD Billions): 2018-2025

Figure 4. Exports of Chinese electric vehicles by region (USD Billions): 2018-2025

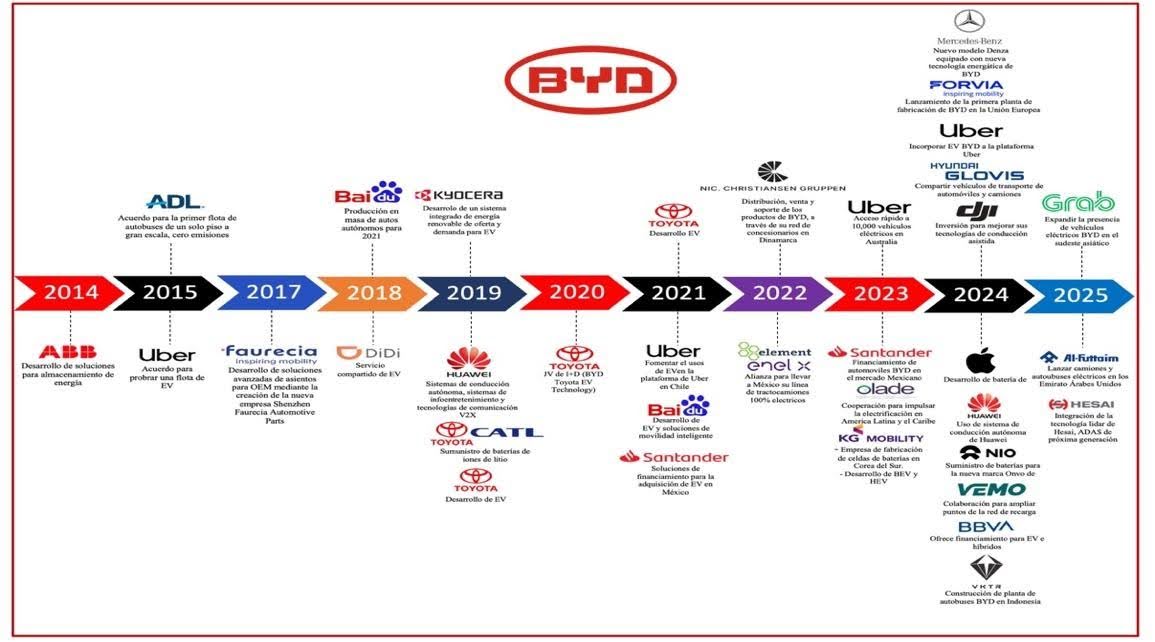

In parallel, the global automotive industry has experienced a growing proliferation of technological and productive alliances among firms of different national origins. These arrangements operate within dynamics of competitive cooperation that reflect the sector’s technological complexity and the need to share risks and capabilities, thereby constituting an ecosystem of intensified competition. Figure 5 illustrates this pattern through the case of BYD – the world’s leading producer of electric vehicles – by mapping the alliances formed over the past decade. These partnerships range from financial institutions and mobility platforms to major technology firms such as Apple and Huawei, adding an additional layer of complexity to contemporary productive dynamics. At the same time, such alliances introduce new vulnerabilities and tensions, particularly in a context of escalating strategic, political, and technological rivalry between China and the United States. Taken together, the shift in productive leadership, the centrality of electrification, and the consolidation of vertically integrated structures help explain why the automotive industry has emerged as a key arena of strategic competition at the global level.

Figure 5: Technological Alliances in the Automotive Industry: 2014-2025

The United States-China Confrontation: Industrial Policy, National Security, and Competing Strategies

The automotive industry constitutes a central arena in the China-United States rivalry, as it brings together industrial capabilities, technological control, and access to critical inputs – dimensions that are increasingly interpreted by the United States through a national security lens. China’s rise as the world’s leading producer and exporter of vehicles, as well as its leadership in batteries and electric vehicles, as argued by Álvarez and Marquina (2023), reflects a long-term strategy grounded in active industrial policies, selective subsidies, technological planning, and control over strategic segments of global value chains. This strategy has been institutionalized through initiatives such as Made in China 2025 and the Internet Plus Action Plan, which seek both to narrow technological gaps and to integrate digital technologies with industrial development.

In response to China’s productive and technological ascent, the US National Security Strategy published by the White House in late 2025 emphasizes supply chain security, productive reshoring, and control over critical inputs – including energy, strategic minerals, and key technologies – as indispensable conditions for preserving economic leadership and safeguarding national security (The White House, 2025). This framework legitimizes the intensive use of protectionist instruments such as tariffs, technological restrictions, and regional content requirements, which are increasingly applied extraterritorially to trading partners embedded within US-centered production networks.

The implementation of the Inflation Reduction Act (IRA) of 2022 – aimed at restricting the entry of Chinese vehicles and inputs – together with the tariff escalation initiated during the Trump administration and intensified in 2025, further reinforces this protectionist logic. While these national security-driven measures seek to contain China’s advance in sectors deemed strategic, they also generate structural tensions by increasing the cost of key inputs and limiting access to low-cost components. This dynamic affects not only Chinese firms but also US companies with production or assembly operations in China and Mexico (Valderrey and Cabrera, 2024; Forbes, 2024). In this sense, the US national security strategy not only redefines relations with China but also reshapes the functioning of regional and global automotive supply chains.

Beyond altering the economic and productive order through tariff threats and trade restrictions, the US security strategy has broader geopolitical implications, insofar as it increasingly frames control over resources as a legitimate justification for military intervention and the exercise of both hard and soft power. Recent military actions in Nigeria and Venezuela have been interpreted by some analysts as expressions of this logic, aimed at securing access to critical inputs and constraining China’s expanding economic influence. In Nigeria, the airstrike of December 26, 2025 – officially justified as a counterterrorism operation against the Islamic State and accompanied by an expanded US military presence across West Africa – has been situated within the context of growing competition over strategic minerals such as lithium, rare earth elements, and manganese, all of which are essential for batteries, clean technologies, and military applications. The availability of these resources has attracted substantial Chinese investment in the country over the past decade (Canuto and Emran, 2025; Impakter, 2025; JD Supra, 2025). This dynamic also suggests that US strategic behavior in other regions and countries – such as Venezuela, Iran, Greenland, or Cuba – may respond to similar logics of resource access and geopolitical positioning, aimed at preserving hegemonic influence and maintaining a strategic advantage over China. From this perspective, the linkage between counterterrorism, supply security, and geopolitical repositioning acquires a structural character.

A similar interpretation can be applied to the military deployment in Venezuela on January 3, which culminated in the capture of President Nicolás Maduro. As noted by Maher et al. (2026), this intervention has been understood not only as a coercive response to a regime portrayed as a threat to US national security, but also as a direct challenge to China’s strategic interests in the South American country. Since 1946 – and with increasing intensity in recent decades – the bulk of Venezuelan oil exports has been directed toward the People’s Republic of China, while Chinese firms have financed large-scale infrastructure and investment projects through oil-backed lending arrangements involving billions of dollars (Brandt and Piña, 2019; Piña, 2019). Given that Venezuela possesses the world’s largest proven crude oil reserves, these dynamics reinforce interpretations that US military action was also motivated by the strategic reconfiguration of control over critical energy supplies.

Taken together, these cases illustrate how the expansion of the US concept of national security extends well beyond the economic and commercial spheres, directly affecting international stability and placing strain on core principles of international law by normalizing the use of force as a means of securing strategic inputs. In contrast, China’s approach toward Latin America and the Caribbean (LAC), articulated through the publication of its Third White Paper on the region, advances a discursive and programmatic framework centered on economic cooperation, productive integration, and the development of shared industrial chains. The document emphasizes respect for sovereignty, non-interference, and the peaceful resolution of disputes, while promoting cooperation in advanced manufacturing, energy, infrastructure, and technology – thus advancing a multilateral orientation (Ministry of Foreign Affairs of the PRC, 2025). From this perspective, China frames its relationship with LAC as complementary and non-confrontational toward third countries, in explicit contrast to the securitized approach underpinning US policy.

These opposing strategies generate significant, albeit indirect, effects for Mexico. On the one hand, US pressure to limit China’s presence in strategic sectors creates an environment of uncertainty that affects not only Chinese firms but also companies from other countries integrated into North American automotive value chains. On the other hand, China’s cooperation-oriented strategy encounters structural constraints derived from Mexico’s deep productive integration with the United States under the USMCA framework, as well as from preexisting industrial alliances, as documented by Dussel Peters (2021, 2025) in his analysis of trilateral relations among the three countries.

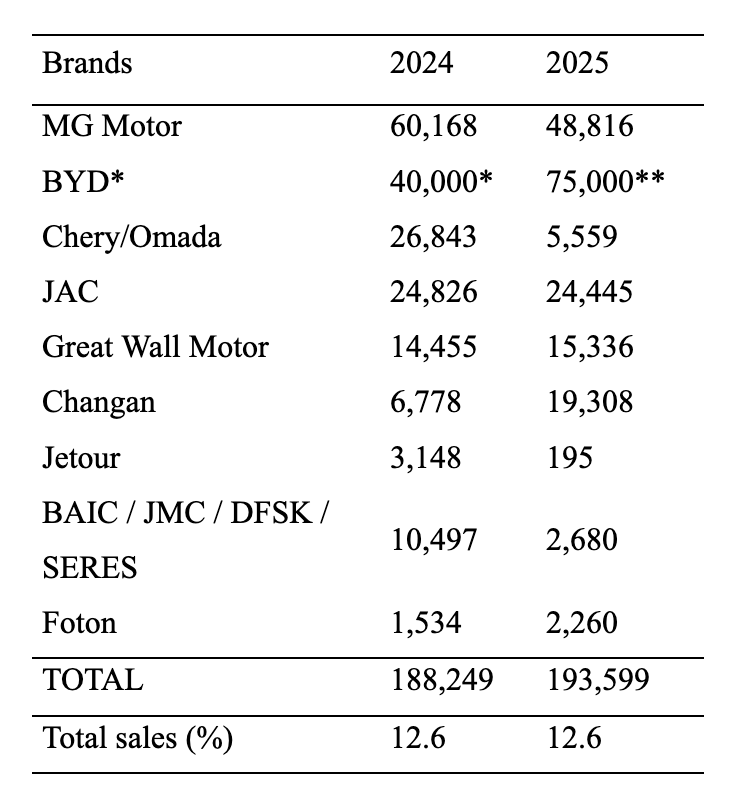

Against this backdrop, it is important to note that the perception of China as a major competitive threat in the US is not reflected in the Mexican market, where Chinese imports have not significantly displaced other producers. Chinese automotive firms’ presence in Mexico remains overwhelmingly concentrated in domestic sales, with no significant export orientation. According to INEGI data, foreign brands such as Nissan and General Motors dominated the Mexican market in 2024, each selling more than 200,000 units (Martínez, 2025), far exceeding the combined sales of all registered Chinese firms, which together reached only 188,249 units in the same year (see Table 1).

Table 1: Light Vehicles: Sales of Chinese Brands in Mexico

Notes: According to INEGI, BYD does not report official figures. Data for 2025 were published on January 9, 2026, in Revista Negocio Motor, edited by Lulú Sierra

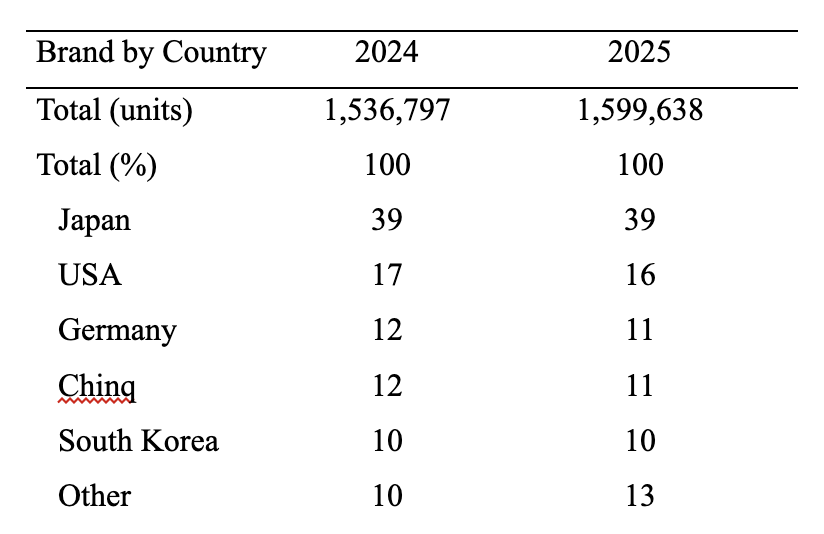

Likewise, Table 2 shows that the overall structure of the Mexican automotive market remains dominated by brands of Japanese, US, and German origin. This configuration suggests that the US response is driven less by the risk of immediate displacement in the Mexican case than by broader, long-term geopolitical and technological considerations.

Table 2: Vehicle Sales in the Mexican Market, 2024-2025, by Country (Units and %)

Finally, the expansion of the US concept of national security to encompass control over critical inputs, strategic technologies, and logistical routes introduces an additional source of systemic uncertainty. Beyond the automotive sector itself, this logic disrupts the regular functioning of global supply chains and disproportionately affects highly integrated economies such as Mexico’s. Although these measures are justified within a security-oriented framework, their effects extend well beyond the commercial sphere, contributing to a volatile international environment with direct implications for investment, technological cooperation, and the overall stability of foreign firms. In this way, these measures decisively condition Mexico’s margins of action.

The Chinese Automotive Presence in Mexico: Conditional Insertion, Incipient Electrification, and Margins of Maneuver

The growth of Chinese automotive firms in Mexico is not an autonomous expansion, but reflects the conditional insertion of a sector that develops within an industrial structure deeply integrated with the United States. In this context, the rules of the USMCA, the historical spatial concentration of automotive clusters, and the export-oriented focus on the North American market delimit the margins of action available to Chinese firms.

In productive terms, Dussel Peters (2021, 2025) observes that the automotive and auto parts sector accounts for the largest share of Chinese investment in Mexico, representing 34 percent of total Chinese investment between 2020 and 2024. This investment has been incorporated into Mexican industry through specific and limited linkages – such as partial assembly, auto parts supply, logistics, and commercialization – without translating into control over complete production platforms or the development of large-scale projects oriented toward export markets. As a result, the structure of the Mexican automotive industry continues to be dominated by traditional assemblers of US, Japanese, South Korean, and German origin, constraining the prospects for deep Chinese insertion in the short term.

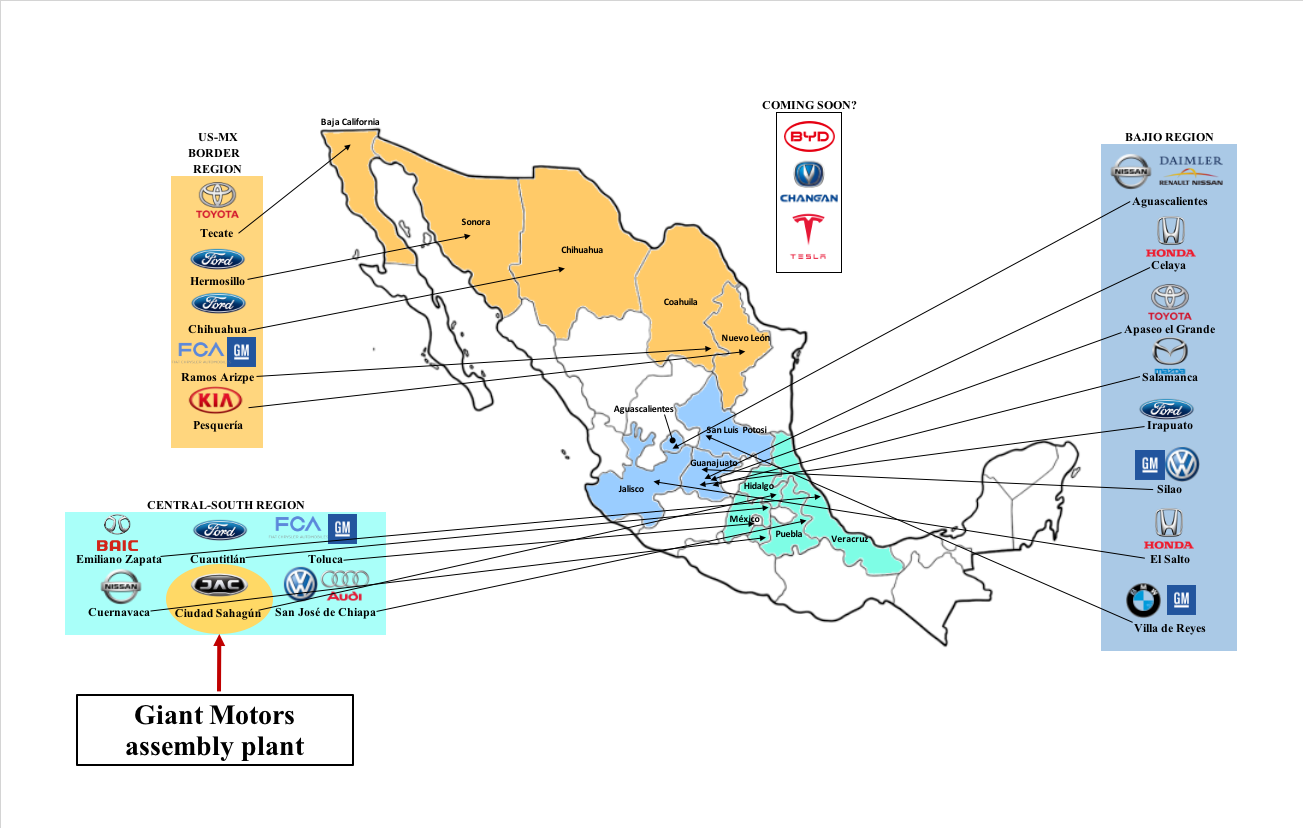

This subordinated form of insertion is also evident at the territorial level. Figure 6 maps the automotive assembly plants currently operating in Mexico and clearly illustrates the dominance of established foreign brands. Until June 2025, only two Chinese firms – JAC and BAIC – have established assembly operations within Mexican territory, underscoring the limited and highly selective nature of China’s productive presence in the country.

Figure 6: Assembly Plants in the Mexican Automotive Industry: 2025

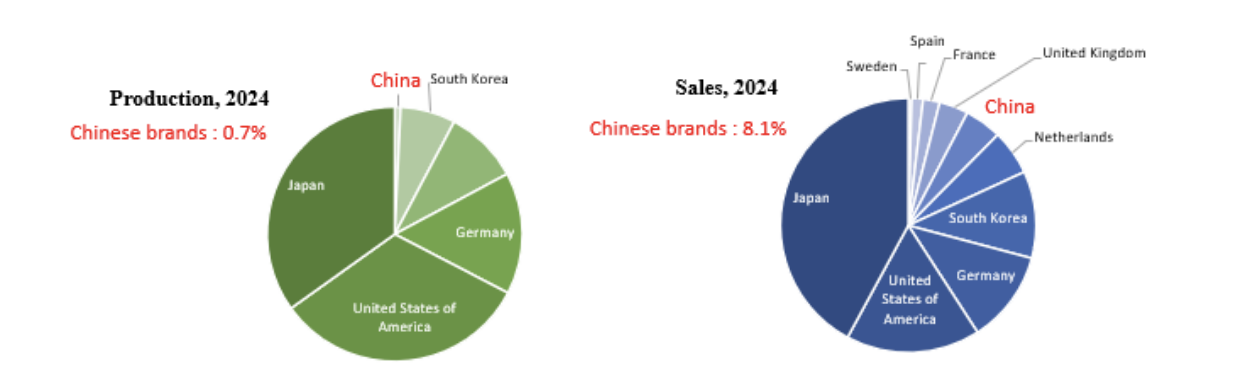

Likewise, the evidence shows that Chinese firms tend to locate within already consolidated automotive clusters, without generating a significant redistribution or expansion of Mexico’s industrial geography. Other firms – such as Changan and BYD – have so far limited their presence to announced investment intentions, without having consolidated production operations. Nevertheless, these dynamics point to a gradual, albeit limited, diversification of the Mexican market, which becomes most visible in the transition toward electromobility. Figure 7 presents electric-vehicle production and sales in Mexico, suggesting that the electrification of the national market – still highly marginal – is advancing only slowly, remaining below 1 percent in terms of production and reaching just 8.1 percent of total sales. These figures remain low when compared with production levels in countries such as the United States and Japan. Overall, this evidence reinforces the conclusion that, to date, the Chinese automotive presence in Mexico has been sustained primarily through domestic market participation rather than export-oriented production.

Figure 7: EV Production and Sales in Mexico

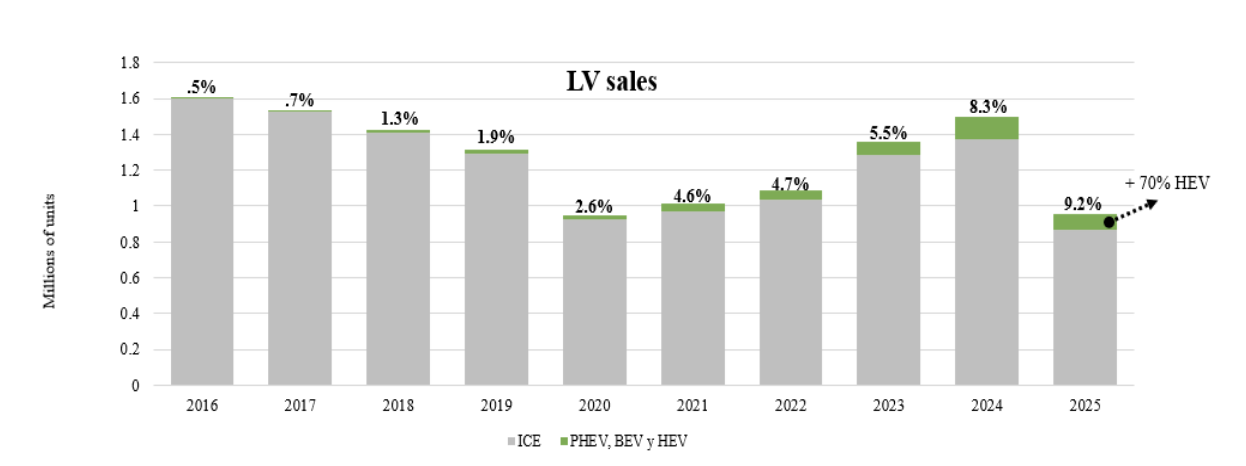

With respect to EV sales, non-plug-in hybrid electric vehicles (HEVs) continue to dominate the Mexican market. These vehicles rely primarily on gasoline and make more limited use of electricity than plug-in hybrid electric vehicles (PHEVs), which require external charging to achieve a greater electric driving range, as well as battery electric vehicles (BEVs), which are fully dependent on electricity. Although HEV sales have increased in recent years, in 2025 they accounted for only 9.2 percent of total vehicle sales across all brands operating in the Mexican market (Figure 8). This pattern underscores the limited penetration of fully electric vehicles in both production and sales, in sharp contrast to China’s global leadership in electromobility, and reinforces the conclusion that Mexico has yet to emerge as a strategic platform for the production of Chinese EVs.

Figure 8: Percentage Shares of of EV Sales in Mexico (all brands): 2025

Consequently, the technological transition of Mexico’s automotive sector faces significant constraints related to infrastructure, costs, regulatory frameworks, and external technological dependence. To date, these conditions have not generated an environment sufficiently conducive to large-scale investments in fully electric platforms, thereby limiting the depth of Chinese insertion. This situation is further compounded by pressure from the United States in the form of tariffs, stricter rules of origin, and economic security criteria, all of which have increased the risks associated with new automotive investments in Mexico and may intensify further in the context of a potential renegotiation of the USMCA. Even US and European firms operating in Mexico face growing tensions as a result of this strategy, reinforcing a generalized climate of caution – particularly given that a substantial share of EVs, including models such as Tesla’s Model 3 and the Mustang Mach-E, incorporate up to 51 percent Chinese content in their manufacturing processes (Forbes, 2024).

Additional sources of internal uncertainty further compound this context, including Plan México, proposed by the administration of President Claudia Sheinbaum, as well as the recent increase in tariffs imposed by Mexico on imports of Chinese products. These measures reveal, to some extent, an alignment with Washington’s broader anti-China strategy. On December 10, 2025, the Mexican Senate approved a set of reforms imposing tariffs on 1,463 imported products and, for the first time, levying duties on 316 goods originating from China, Vietnam, India, and other Asian countries. The affected products include auto parts, plastics, trailers, and aluminum, among others, with direct implications for the automotive industry. These measures have already generated immediate tensions: China’s Ministry of Commerce warned that they would “substantially harm” Mexican trade, while President Trump repeatedly accused Mexico of acting as a “back door” for products originating in China (Nicas and Wagner, 2025).

Plan México, for its part, proposes reducing imports – particularly from China – by up to 50 percent, cutting administrative procedures by half, and increasing domestic production of inputs within global value chains linked to sectors such as automotive manufacturing, electronics, and semiconductors (Secretaría de Gobernación, n.d.). While these objectives are intended to stimulate domestic manufacturing, they also risk restricting access to key inputs for automotive assembly, potentially undermining production volumes, domestic consumption, and export competitiveness. All of this unfolds under continued external pressure stemming from the tariff conflict driven by the Trump administration and its efforts to maintain control over critical inputs, thereby introducing additional uncertainty regarding new investment inflows, the expansion of industrial parks, and the continuity of trilateral automotive trade flows.

Taken together, the Chinese automotive presence in Mexico is best characterized as a form of constrained diversification – more visible in commercial activities and supply provision than in productive investment – and strongly conditioned by both internal and external factors. Mexico thus does not emerge as a space for unrestricted expansion, but rather as an intermediate territory in which opportunities coexist with geopolitical, technological, and regulatory constraints. This confirms that China’s presence should be understood less as an immediate threat to the United States than as a structurally conditioned phenomenon, whose effective margins of development are defined by the global balance of power and by domestic industrial policy choices.

Conclusion

The reconfiguration of the global automotive industry confirms that the transition toward electromobility and the control of critical inputs have become central axes of China-United States competition. China’s leadership in the production of electric vehicles, batteries, and key segments of the value chain is not driven solely by cost advantages, but rather by a long-term industrial strategy that has reshaped international production structures and intensified the securitization of US economic policy.

The expansion of the US concept of national security has, in turn, generated an environment of growing uncertainty for global and regional automotive value chains. The combined use of tariffs, stricter rules of origin, technological controls, and the normalization of securing critical inputs as strategic objectives has produced disruptions that extend beyond the commercial sphere and affect the stability of the international system as a whole. Within this context, Mexico is particularly exposed due to its deep productive integration with the US economy and its role as a key platform under the USMCA, whose rules may be revised following its scheduled review in July of this year.

The analysis demonstrates that the Chinese automotive presence in Mexico does not constitute an unrestricted expansion or an effective displacement of established actors. Instead, it represents a structurally conditioned form of insertion – more visible in commercial activities than in productive investment – largely concentrated in the domestic market and limited in terms of assembly, supply, and export capacity. At the same time, the slow pace of electrification in Mexico prevents the country, at least for now, from consolidating itself as a relevant platform to produce Chinese EVs, despite these firms’ global leadership in other markets.

These external constraints are compounded by domestic economic policy decisions that further narrow Mexico’s margins of maneuver. The increase in tariffs on electric vehicle imports – reaching deterrent levels of up to 50 percent – together with the orientation of Plan México toward import substitution and the reduction of foreign supply, send ambiguous signals to automotive investors. While such measures seek to strengthen domestic manufacturing, in practice they risk discouraging new investment projects, limiting productive linkages, and deepening Mexico’s structural dependence on the US economy.

Finally, this study argues that Mexico faces a strategic dilemma. The country’s growing alignment with the United States, within a context of open rivalry with China, constrains opportunities for productive and technological diversification in the automotive sector. This dynamic reinforces a form of structural dependence that, rather than being resolved, tends to intensify under the current development model. Nevertheless, as Dussel Peters (2025) suggests, Chinese investment should not be understood as a substitute for flows originating from the United States, Canada, the European Union, or other Asian economies, but rather as a potential complement capable of contributing to the modernization of Mexico’s productive apparatus – particularly in the automotive industry and in electromobility-related technologies, where Chinese firms are at the technological frontier. Looking ahead, it is therefore urgent to advance toward an intelligent diversification strategy that expands productive capacities, reduces vulnerabilities, and strategically leverages the relationship with China – not as a replacement for North American integration, but as a component of a more balanced industrial development path. The realization of this potential will ultimately depend on the Mexican state’s capacity to redefine its industrial strategy in an environment marked by interdependent strategic competition, accelerated electrification, and pervasive global uncertainty.

References

Álvarez, M. y Marquina, L. (2023). “Instrumentos de política pública para la adopción de vehículos eléctricos en China.” In E., Dussel Peters (Coord.), América Latina y el Caribe - China: Economía, comercio e inversión 2023 (pp. 149-176). Red ALC-China/ UNAM.

Brandt, C. y Piña C. E. (2019). Las relaciones Venezuela-China (2000-2018): entre la cooperación y la dependencia. Friedrich Ebert Stigfund Venezuela. https://www.academia.edu/42171297/Las_relaciones_Venezuela_China_2000_2018_entre_la_cooperaci%C3%B3n_y_la_dependencia

Canuto, O. & Emran, S. (2025). Africa's Minerals Will Shape the Future of Global Power. Project Syndicate.

https://www.project-syndicate.org/commentary/race-for-african-minerals-could-determine-who-wins-us-china-tech-rivalry-by-otaviano-canuto-and-sabrine-emran-2025-04

Cheng, S. y Kubota, Y. (March 4, 2024). How China Is Churning Out EVs Faster Than Everyone Else. The Wall Street Journal.

https://www.wsj.com/business/autos/how-china-is-churning-out-evs-faster-than-everyone-else-df316c71

Congressional Research Service. (2025). Section 232 tariffs on automobiles and automobile parts (CRS Report No. R48549). US Congress. https://www.congress.gov/crs-product/R48549

Dupuis, M., Greer, I., Kirsch, A., Lechowski, G., Park, D. y Zimmermann, T. (2024). A Just Transition for Auto Workers? Negotiating the Electric Vehicle Transition in Germany and North America. ILR Review, 77(5), 770-798. https://doi.org/10.1177/00197939241250001

Dussel Peters, E. (2021). The New Triangular Relationship between the US, China, and Latin America: The Case of Trade in the Autoparts-Automobile Global Value Chain (2000-2019). Journal of current Chinese affairs, 51(1), 60-82. https://doi.org/10.1177/18681026211024667

Dussel Peters, E. (2025). México ante el security-shoring y la confrontación entre Estados Unidos y China. Condiciones y desafíos ante las inversiones chinas. Norteamérica, Revista Académica Del CISAN-UNAM, 20(2). https://doi.org/10.22201/cisan.24487228e.2025.2.755

Esparza, Z. (2008). China: el nuevo gigante automotriz. México y la Cuenca del Pacífico, 11(33), 57-71. https://www.redalyc.org/articulo.oa?id=433747603004

Ewing, J. (Jan. 2, 2026). China’s BYD Surpasses Tesla as World Leader in Electric Car Sales. The New York Times.

https://www.nytimes.com/2026/01/02/business/tesla-electric-vehicles-fourth-quarter-sales.html

Forbes. (2024, 14 de mayo). La guerra comercial entre Estados Unidos y China amenaza la agenda de autos eléctricos de Biden.

https://forbes.com.mx/la-guerra-comercial-entre-estados-unidos-y-china-amenaza-la-agenda-de-autos-electricos-de-biden/

García, G. (November 26, 2025). BYD habla claro: no abrirá una fábrica en México, pero sí tiene otros planes para 2026. Motorpasíon México.

https://www.motorpasion.com.mx/industria/byd-habla-claro-no-abrira-fabrica-mexico-tiene-otros-planes-para-2026

García, M. (January 09, 2026). Industria automotriz mexicana cierra 2025 con 3.95 millones de vehículos producidos y 3.38 millones exportados. Cluster Industrial.

https://clusterindustrial.com.mx/industria-automotriz-mexicana-cierra-2025-con-3-95-millones-de-vehiculos-producidos-y-3-38-millones-exportados/

Carrillo, J. y Gomis, R. (2026). Fabricantes de autos y gigantes tecnológicos. Alianzas para la nueva movilidad. El COLEF.

Instituto Nacional de Estadística y Geografía [Inegi]. (2026). Registro Administrativo de la Industria Automotriz de Vehículos Ligeros (RAIAVL). INEGI. https://www.inegi.org.mx/datosprimarios/iavl/#datos_abiertos

International Energy Agency [IEA]. (2024). Global EV Outlook 2024. Moving towards increased affordability.

https://iea.blob.core.windows.net/assets/a9e3544b-0b12-4e15-b407-65f5c8ce1b5f/GlobalEVOutlook2024.pdf

International Energy Agency [IEA]. (2025). Global EV Outlook 2025. https://www.iea.org/reports/global-ev-outlook-2025

JD Supra. (2025). Hot topics in international trade. https://www.jdsupra.com/legalnews/hot-topics-in-international-trade-7326371/

Maher, K., Collins, K. y Godman, D. (7 de enero de 2026). Trump afirma que Venezuela entregará entre 30 y 50 millones de barriles de petróleo a EE.UU. CNN. https://cnnespanol.cnn.com/2026/01/06/venezuela/entregar-30-50-millones-barriles-petroleo-eeuu-trax

Martínez, B. (January 08, 2025). Ventas de autos en México 2024: ¿Qué marca vendió más autos? El Universal.

https://www.eluniversal.com.mx/autopistas/ventas-de-autos-en-mexico-2024-que-marca-vendio-mas-autos/

Mazzoco, I. (November 19, 2025). The Internationalization of China’s Automotive Sector”, Nov 19, Auto Future Seminar, 2025.

https://sites.google.com/umich.edu/automotivefutures/conferences/2025-conferences/2025-inside-china-auto-conference

Ministerio de asuntos exteriores de la RPCh. (2025). Documento sobre la Política de China Hacia América Latina y el Caribe.

https://spanish.xinhuanet.com/20251210/e2dec9c6d13b4802919c7a7d87b0ecb5/

20251210e2dec9c6d13b4802919c7a7d87b0ecb5_XxjwssS000010_20251210_CBMFN0A001.docx

Navarrete, F. (January 10, 2025). La producción y la exportación de autos suben 5.6 y 5.4% anual. El Financiero.

https://www.elfinanciero.com.mx/empresas/2025/01/10/la-produccion-y-la-exportacion-de-autos-suben-56-y-54-anual/

Nicas, J. y Wagner, J. (December 11, 2025). México se compra el pleito de Trump: pone aranceles a China y otros países asiáticos. The New York Times.

https://www.nytimes.com/es/2025/12/11/espanol/america-latina/mexico-aranceles-china.html

Organisation Internationale des Constructeurs d'Automobiles [OICA]. (2026). Production Statistics. https://oica.net/production-statistics/

Piña, C. E. (2019). “Chinese financing in Venezuela.” En E. Dussel Peters (ed.), China’s financing in Latin America and the Caribbean (pp. 337-371). CECHIMEX-UNAM.

Secretaría de Gobernación. (s.f.). Plan México. Estrategia de Desarrollo Económico Equitativo y Sustentable para la Prosperidad Compartida. Primer borrador. https://www.planmexico.gob.mx/

Seifman, R. (2025). Trump’s ‘America First’ Policy in Africa: The Consequences. Impakter Business of Sustainability.

https://impakter.com/trumps-america-first-policy-in-africa-the-consequences/

Sierra, L. (January 09, 2026). BYD México coloca 75 mil autos en 2025; inicia fase Consolidación 2026. Revista Negocio Motor.

https://www.negociomotor.com.mx/post/byd-m%C3%A9xico-coloca-75-mil-autos-en-el-2025-inicia-fase-consolidaci%C3%B3n-2026

The White House. (2025). National Security Strategy of the United States of America.

https://www.whitehouse.gov/wp-content/uploads/2025/12/2025-National-Security-Strategy.pdf

Valderrey, F. J. y Cabrera, J. G. O. (2024). “Impacto del nearshoring en las relaciones México-China.” En E., Dussel Peters (Coord.), América Latina y el Caribe y China. Economía, comercio e inversión 2024 (pp. 13-33). CECHIMEX-UNAM.

You, X. (November 17, 2025). Cómo China ganó con sorprendente rapidez la carrera mundial por las baterías para vehículos eléctricos. BBC. https://www.bbc.com/mundo/articles/c1m3v5z0r3ko